As such, the combined potash production of Russia and Belarus in 2020 was 38% of global supply, exceeding Canada's 32% of global production. Russia and Belarus are low-cost producers who have recently been content to ship larger volumes at lower prices. In fact, “SIA Uralkali trading” a subsidiary of Uralkali based in Latvia had the largest turnover of any company in Latvia in 2020: 1.81 billion euros, but reported a loss of 90.48 million euros.

In the context of overall economic impact potash exports are particularly important to Belarus and constitute around 9% of their annual exports.

This is why we anticipated that potash exports would be the target of western sanctions after the political repressions following the August 2020 Belarusian presidential elections and hijacking of Ryanair flight 4978 of last summer. We also knew that sanctioning 18% of the global production of any commodity will resultingly have a massive impact on price.

At the start of February of this year, Lithuania banned the transport of Belarusian potash through its terminal in Klaipeda, ostensibly stranding Belarusian potash exports. When Putin invaded Ukraine, the situation in the potash market became unprecedented in terms of supply dynamics. Now Russia's exports would be constrained as well and would have to scramble to find new port capacity, arrangements, and even end buyers.

But what is potash and why is it important?

The term "potash" refers to a group of potassium (K) bearing minerals and chemicals.

According to Canpotex, potassium improves a plant's overall health and boosts crop yields. Potash is important for agriculture because it improves water retention, yield, nutrient value, taste, color, texture and disease resistance of food crops. It has wide application to fruit and vegetables, rice, wheat and other grains, sugar, corn, soybeans, palm oil and cotton, all of which benefit from the nutrient's quality-enhancing properties.

Potassium is one of three essential elements for plant growth, the others being Nitrogen, which helps a plant's leaves grow, and phosphorus, which supports a plant’s root growth and flower and fruit development.

The improvement of fertilization application has enabled a massive growth in global crop yields since the Second World War and enabled an unprecedented explosion of the world's population, especially in emerging markets.

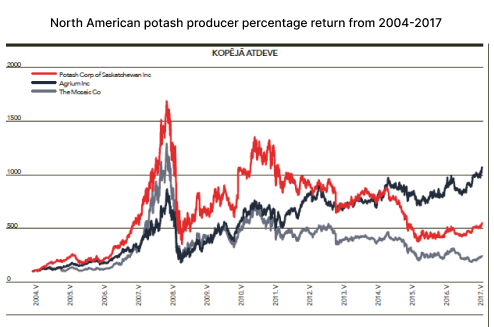

During the 2000s, the attention of global investors was fixated on supplying the growing demands of the consumers of emerging Asia, and China in particular. One of the most powerful narratives prior to the Great Financial Crisis was that the first thing that the Chinese would do as they gained more disposable income would be to eat more meat – long considered to be an unattainable luxury under the communist regime.

It was calculated that every kilogram of chicken raised would require 2.5 kilograms of feed. A kilo or pork would require around 4x as much feed and beef up to 7x times more feed.

This suggested an unprecedented demand for agricultural commodities, and Canpotex and BPC controlled 70% of the production of an essential element for raising crop yields.