At zero EURIBOR and a 2.5% financing rate (some of you might have mortgages as low as 2%...), monthly payment for a 100 000 euro mortgage would have been 400 euro per month. If the ECB raises its Main Refinacing Rate to 3.5% your total effective interest rate will be at least 6% (3 month EURIBOR will be higher than the Main Refinancing Rate). Under such conditions, your monthly payment would rise to 600 euro per month – a 50% increase. This is problematic given that the average net salary in Latvia is 1000 euro per month after taxes. Therefore in order to combat inflation levels that recently exceeded 20% in Latvia, we will have to pay 50% more for our monthly mortgage payments. And this of course does not make any consideration for higher electricity and heating costs this winter.

Central bankers are supposed to be sober individuals that act in accordance to data. They take themselves very seriously. So how did we ended up where we are now? What can be done about it? And how should clear sighted investors position themselves?

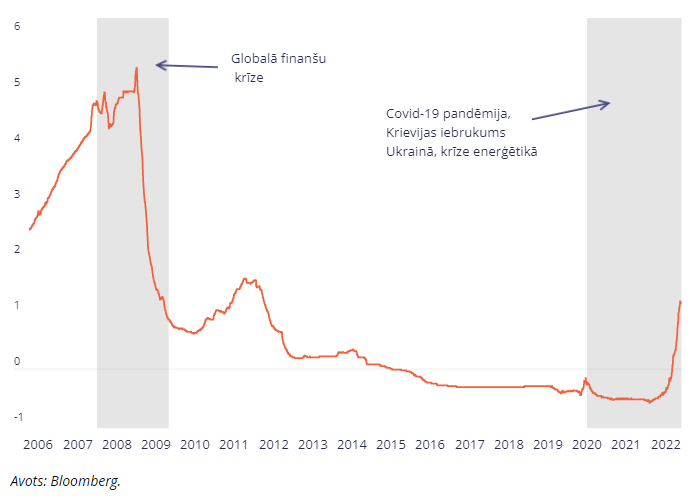

The foremost question that comes to mind given this bewildering central banker inflation drama is how institutions that are so powerful, can present themselves to be so powerless when facing the consequences of their own actions? Just as importantly, why do they persevere in intimating that it is our fault? That consumers are consuming too much. I recently read an article from the Bank of Latvia’s portal makroekonomika.lv (“Cik augstas procentu likmes sagaidīt nākotnē?) that glibly pointed out that the recent move in rates is not so bad compared to EURIBOR during the Great Financial Crisis. Really? That is your chosen point of comparison?

Then again, it matters not. What is done is done, and central banks will keep going until they stop. They are influential. You, humble investor, are not. When they speak, it pays to listen. Until it doesn’t.

According to central bankers inflation is the enemy. Here they have a point. High inflation punishes savers and creates uncertainty in terms of economic expectations. Although they created a money supply bonfire that was ignited by the monetary equivalent of a flame thrower during Covid lockdowns, they continue to stick to the narrative that there is too much demand, and that they must raise rates to suppress this demand.

Unfortunately their narrative ignores the other side of the holy equation upon which all modern economics is based. According to central bankers, too many people want nice things, so they must crush demand to reassert a reasonable equilibrium. They seldom make any reference to the true problem: supply.

Inflation sparked up during the later stages of Covid, not because of demand, but because there were supply disruptions. We had money, but we did not have the ‘stuff’ that we not only wanted, but needed.

Interest rates were at record lows for the past eight years, yet somehow all this free money could not find its way to expanding production or a least finding a way to safeguard us from an exorbitant rise in the cost of production of things we actually need. This has been revealed to be policy error of the highest order - especially in the energy market. Central bankers are not to blame for a lack of prudent and constructive economic policy, but their overly loose monetary policy enabled the inflation of a financial asset bubble, real estate prices in many major markets, and even fueled a virtual asset extravaganza.

But here’s the thing: there are four major issues with central bankers’ plans to curtail inflation by raising rates.

First of all, they can only force down demand for so long. Political cycles are too short and central bankers are not independent and we should stop pretending that they are.

Politicians gain power by promising prosperity. This will put pressure on central bankers to stop raising rates. Once they do, markets will adjust and life will go on under a new reality. Inflation will continue to be higher that the central bankers’ desired rate of 2%.

Secondly, higher rates make capital more expensive which means that they will disincentivize new supply and too much money will continue to chase scarce goods.

Thirdly, central bankers actually secretly want inflation because it is the only thing that will bring down the present value of the future liabilities that they have taken on by issuing such staggering amounts of debt. They just can’t admit it. Not publically.

Lastly, by raising rates, central banks make refinancing government debt more expensive. With their most recent rate raise, the US Fed interest rate policy will actually result in the US Treasury losing money. The higher they go, the more they will cost the US government and this will not go unnoticed. Currently this only effects newly issued debt, but with time this will create a larger and larger burden.